For years, the crypto industry has used the names “XRP” and “Ripple” almost interchangeably. Financial media often refers to XRP as “Ripple,” traders discuss Ripple price movements while actually referring to XRP, and many retail investors assume both are the same organization operating under one structure.

However, the reality is far more complex.

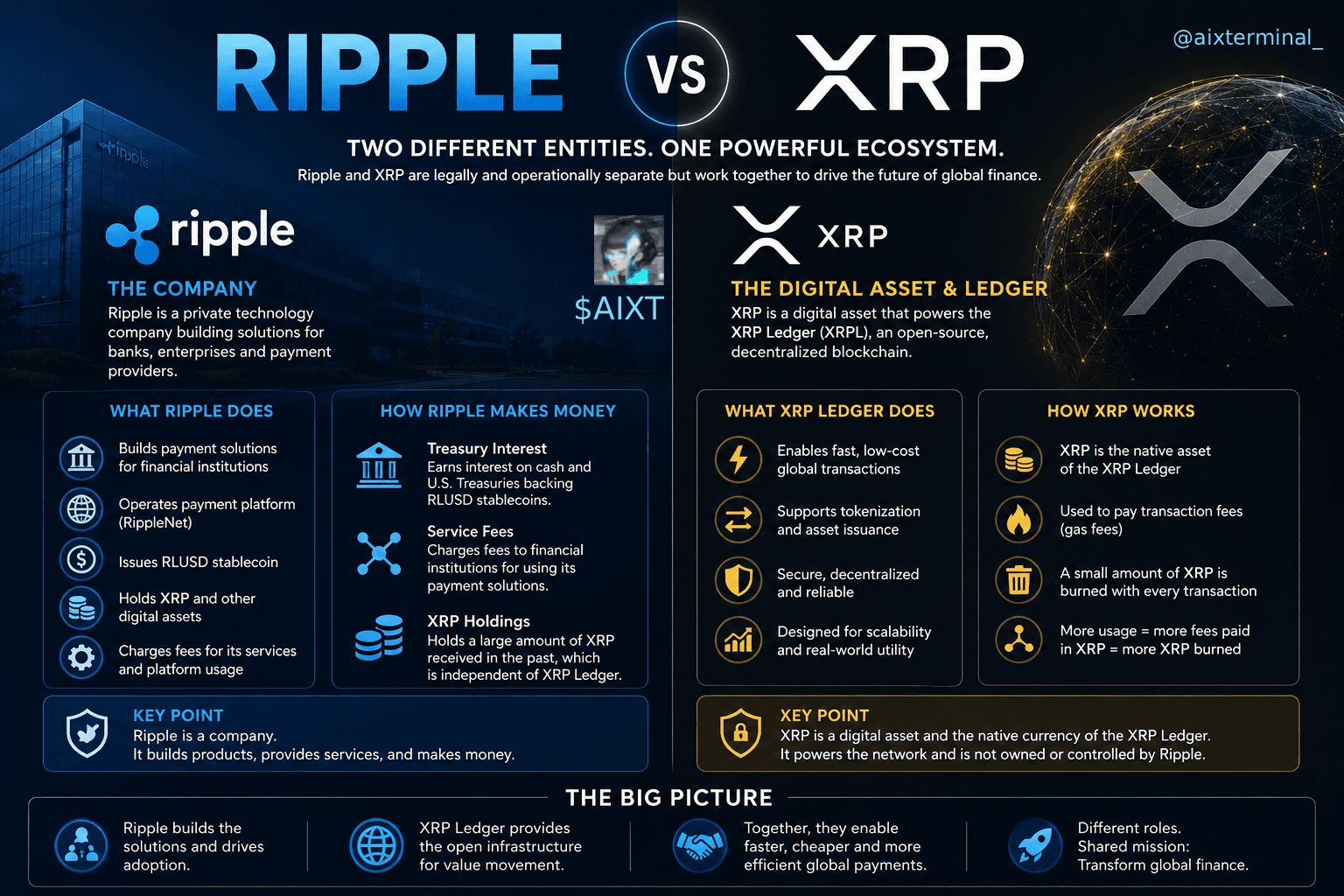

XRP and Ripple are legally separate entities that operate with different purposes, different economic models, and different ways of generating value. Understanding this distinction is important because many misconceptions surrounding XRP’s long-term value stem from confusion between Ripple’s business success and the XRP Ledger’s actual mechanics.

This article explores how Ripple and XRP function separately, how transaction “lanes” inside the ecosystem can work, where revenue is generated, and why many XRP holders debate whether Ripple’s growing stablecoin business truly benefits XRP itself.

## The Origins of XRP and Ripple

The XRP Ledger (XRPL) was originally developed in 2012 as a blockchain optimized for high-speed financial transactions. Unlike Bitcoin, which was designed primarily as decentralized digital money, the XRP Ledger focused heavily on payment infrastructure, remittances, liquidity movement, and banking-related transaction efficiency.

Ripple, the company, played a major role in developing and promoting the XRP Ledger in its early years. However, Ripple later structured itself as a legally separate company operating independently from the XRP Ledger itself.

This separation became especially important during years of regulatory scrutiny and legal discussions surrounding digital assets in the United States.

Today:

* Ripple is a private fintech company. * XRP is a digital asset operating on the XRP Ledger blockchain. * The XRP Ledger continues functioning independently of Ripple’s direct ownership.

Although closely associated in branding and ecosystem development, they are technically and legally distinct systems.

## Why the Difference Matters

Many investors assume:

> “If Ripple succeeds, XRP automatically succeeds.”

But this is not always guaranteed.

Ripple can potentially generate significant revenue from:

* payment services, * enterprise banking solutions, * stablecoin operations, * treasury management, * platform fees, * and holdings of XRP itself,

without XRP necessarily appreciating proportionally in value.

This distinction is one of the most debated subjects inside the XRP community.

## Understanding the “Two-Lane” Theory

At the consumer level, the XRP Ledger mostly appears straightforward:

* transactions occur using XRP, * gas fees are paid in XRP, * and tiny portions of XRP are burned during network activity.

This is essentially a “single-lane” transaction system.

However, at the institutional or banking level, the ecosystem becomes more complex.

Some analysts describe XRP Ledger institutional activity as operating through “two lanes.”

While not official terminology from Ripple itself, the concept helps explain how different value layers interact inside the ecosystem.

Lane One: XRP as the Blockchain Fuel

The first lane involves the XRP Ledger infrastructure itself.

Here:

* XRP acts as the native gas token, * transaction fees are paid in XRP, * and a small amount of XRP is permanently burned during transactions.

This mechanism helps:

* prevent spam attacks, * maintain network efficiency, * and slowly reduce XRP supply over time.

However, XRP transaction fees are extremely small.

This creates an important debate:

* high transaction volume increases utility, * but low fees mean very little XRP is burned relative to total supply.

## XRP Burn Economics

Currently, approximately 56 billion XRP are circulating in the market.

Even if network activity became extremely large — for example:

* 10 million transactions per day —

the estimated annual burn rate would still only remove roughly:

* 10 to 15 million XRP annually.

While that sounds significant initially, mathematically it represents only around:

* 0.02% of total circulating supply per year.

At that pace, it would take centuries or even thousands of years for transaction burns alone to dramatically reduce XRP supply.

This means XRP’s long-term value likely depends far more on:

* demand, * adoption, * liquidity usage, * institutional integration, * and market psychology

than on deflationary burn mechanics alone.

## Lane Two: The Actual Money Movement Layer

The second lane is where larger institutional remittance activity may occur.

This is where stablecoins and settlement assets can travel across the XRP Ledger infrastructure.

For example:

* Ripple’s RLUSD stablecoin, * or potentially other digital assets, * can theoretically move through the XRP ecosystem while using XRPL infrastructure underneath.

In this framework:

* XRP powers the network, * while the actual remittance value travels separately.

This distinction is critical.

Many XRP supporters originally believed XRP itself would become the primary bridge asset used for global remittances. However, stablecoins introduce another possibility:

* financial institutions may prefer stable-value assets for settlement, * while XRP mainly handles transaction infrastructure.

## Ripple’s RLUSD Stablecoin Strategy

Ripple recently expanded deeper into stablecoins through RLUSD.

Stablecoins represent one of the most profitable sectors in crypto because issuers typically hold:

* U.S. dollars, * Treasury bills, * short-term government securities, * or cash-equivalent reserves

to back the tokens.

The issuer then collects interest generated from those reserves.

This is the same general business model used by:

* Tether (USDT), * Circle (USDC), * and other stablecoin providers.

If Ripple grows RLUSD adoption substantially, Ripple can potentially generate large recurring revenue streams from treasury interest alone.

This revenue does not necessarily flow directly to XRP holders.

That distinction matters enormously.

## How Ripple Potentially Generates Revenue

Ripple’s business model may include several revenue streams simultaneously.

### 1. Stablecoin Treasury Interest

Ripple can collect interest earned from RLUSD reserve assets.

As RLUSD circulation grows:

* reserve capital grows, * Treasury exposure grows, * and interest income potentially increases.

### 2. XRP Holdings

Ripple historically received large allocations of XRP during the early ecosystem structure.

As XRP’s market value changes, Ripple’s treasury holdings may appreciate significantly.

### 3. Enterprise Payment Services

Ripple also operates payment infrastructure and enterprise-facing financial services.

If institutions use Ripple’s platforms for:

* remittances, * settlement, * liquidity routing, * or blockchain connectivity,

Ripple may collect platform and service fees separately from XRP Ledger transaction fees.

## Does Ripple’s Success Automatically Increase XRP Value?

This is where major community debate exists.

Bullish XRP supporters argue:

* more Ripple usage creates more XRPL activity, * more institutions entering the ecosystem increases XRP visibility, * and XRP eventually benefits from network effects.

Critics argue:

* stablecoins may reduce the need to hold XRP directly, * Ripple can monetize infrastructure without relying heavily on XRP demand, * and transaction fee burns remain too small to meaningfully reduce supply.

In simple terms: Ripple and XRP may benefit each other indirectly, but they do not share identical economic structures.

## Why Banks Might Prefer Stablecoins Over XRP

From a banking perspective, stablecoins provide advantages:

* lower volatility, * predictable accounting, * easier compliance, * reduced FX risk, * and simpler treasury management.

For example:

* moving $100 million through a stablecoin may feel safer operationally than using a highly volatile asset.

This creates another ongoing debate: Will XRP become the dominant settlement asset? Or will XRPL mainly become infrastructure supporting stablecoin-based financial movement?

The answer may determine XRP’s long-term economic role.

## The Bigger Picture

Despite criticism and debates, XRP remains one of the longest-running and most recognized digital asset ecosystems in crypto history.

The XRP Ledger continues offering:

* fast settlement, * low transaction costs, * high throughput, * and strong institutional branding recognition.

Meanwhile Ripple continues expanding:

* banking partnerships, * stablecoin initiatives, * payment infrastructure, * and enterprise blockchain services.

Whether XRP itself becomes massively valuable from these developments remains one of crypto’s most polarizing questions.

## Final Thoughts

The relationship between XRP and Ripple is far more nuanced than many investors realize.

Ripple is a company capable of generating revenue from:

* enterprise services, * stablecoin reserves, * treasury interest, * and platform infrastructure.

The XRP Ledger is a blockchain network where XRP acts primarily as the native transaction and gas asset.

While both systems are connected historically and operationally, they do not function as identical economic entities.

For XRP holders, the core long-term question remains: Will Ripple’s expanding ecosystem ultimately create massive direct demand for XRP itself, or will XRP mainly serve as infrastructure fuel while Ripple captures most of the larger financial upside through services and stablecoin operations?

That debate continues to shape one of crypto’s most fascinating ecosystems.

Note: This article was published on BanxChange.com and is powered by the BXE Token on the XRP Ledger. For the latest articles and news, please visit BanxChange.com